The ACA Tax Credit Cliff: Why Expiring Subsidies Are the Real 2026 Time Bomb

Forget the 2026 elections; the imminent expiration of enhanced ACA tax credits is the silent financial shockwave threatening millions of Americans' health coverage.

Key Takeaways

- •The temporary enhancement of ACA tax credits is set to expire in 2026, threatening massive premium spikes for millions.

- •This impending affordability crisis is the real economic time bomb, overshadowing typical election cycle issues.

- •The political strategy appears to be delaying the pain until the next electoral cycle, shifting blame.

- •Expect forced, last-minute legislation to re-extend subsidies due to inevitable public outcry.

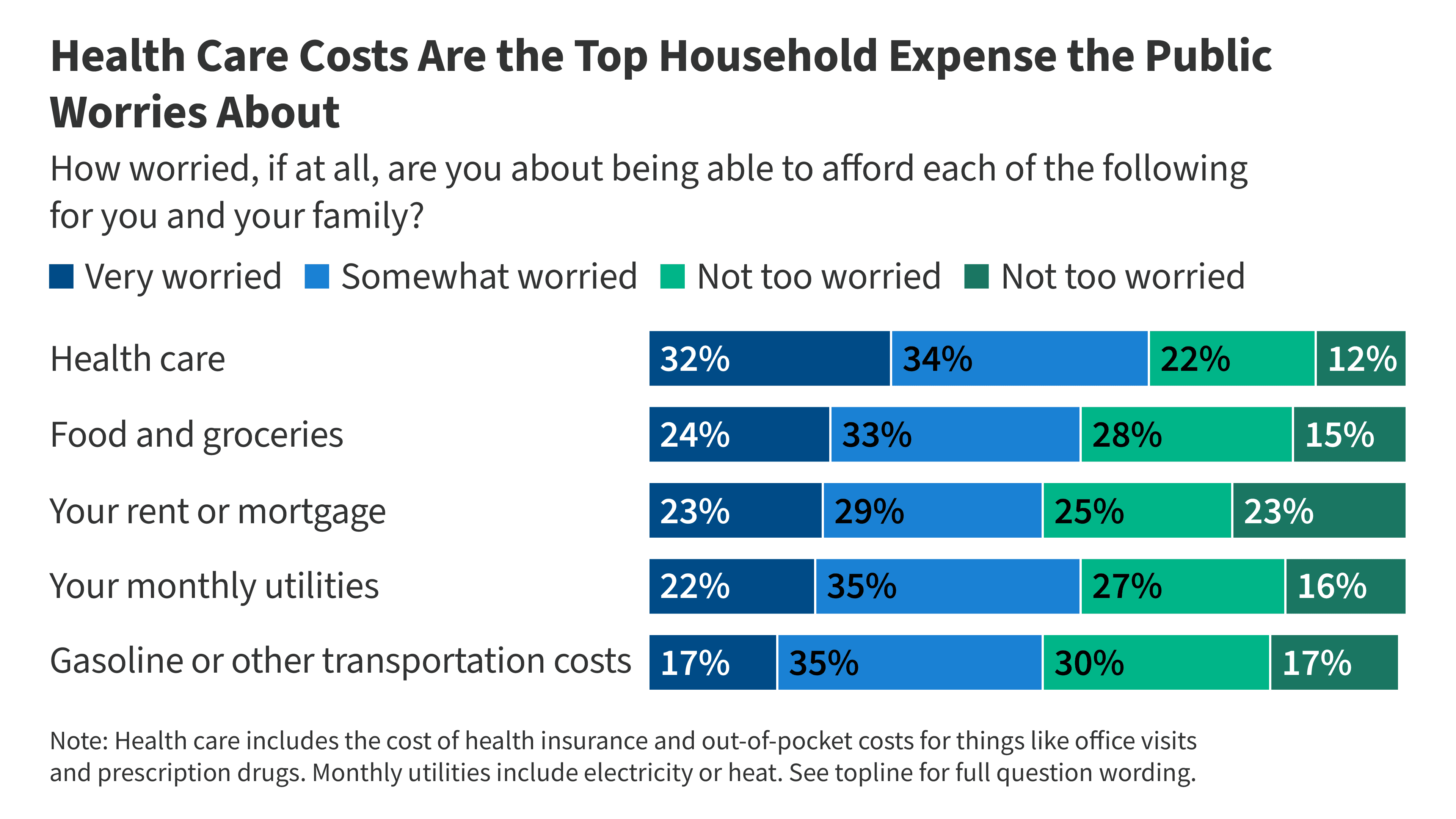

The Unspoken Truth: Healthcare Costs Are the New Mortgage Crisis

The latest KFF tracking poll reveals what every household already knows: healthcare costs are crushing American budgets. But the real story isn't just that premiums are high; it’s the ticking clock attached to the subsidies keeping those premiums affordable. While cable news debates border security and inflation, the political class is studiously ignoring the fiscal cliff looming over the Affordable Care Act (ACA) marketplace in 2026. This isn't just about insurance; it's about the next great economic shockwave for the middle class.

The current enhanced premium tax credits, expanded under the Inflation Reduction Act, have been a lifeline, masking the true underlying cost of American medical care. They made ACA plans look affordable, driving enrollment numbers to historic highs. Now, those enhancements are set to expire. The hidden agenda here is clear: politicians are betting that by the time the subsidies vanish, the ensuing premium spikes will be blamed on the *next* administration, not the architects of the current temporary fixes. This is political cowardice disguised as fiscal prudence.

The 2026 Premium Shock: A Contrarian Take

Everyone focuses on the 2026 midterms as a political reckoning. I argue the real reckoning will be economic. When these temporary subsidies vanish, millions of middle-income families who currently pay pennies on the dollar for coverage will suddenly face premiums that consume 8% to 10% of their income again—or worse. For families earning just above the Medicaid threshold, this sudden jump in health insurance costs will force impossible trade-offs: ditching coverage entirely, downgrading to catastrophic plans, or cutting deeply into other necessities like housing or food.

This isn't a minor adjustment; it’s a policy-induced affordability crisis. The winners in this scenario are not the consumers; they are the insurance companies who can rely on a captive, subsidized customer base, and the politicians who successfully punted the difficult decision down the road. The losers are the millions of Americans who will suddenly see their disposable income evaporate overnight.

Deep Analysis: The Erosion of Public Trust

This pattern—implementing popular, necessary fixes as temporary measures—erodes public trust faster than any single policy failure. When coverage suddenly becomes unaffordable again, the public won't blame the sunset clause; they will blame the entire system. This volatility makes long-term financial planning impossible for average citizens, cementing the perception that healthcare policy is a political football, not a stable safety net. For context on the rising cost burden, look at the historical trends of medical inflation versus wage growth [Reuters Analysis of Health Costs].

Where Do We Go From Here? The Inevitable Re-Subsidization

Prediction: Congress will be forced into emergency legislation in late 2025 or early 2026 to extend these credits, likely at even higher levels, because the political fallout from allowing them to lapse would be catastrophic. However, this extension will be messy, negotiated under duress, and will likely be framed as a 'bailout' rather than a necessary correction. The system is addicted to the subsidy patch, and kicking the can down the road only makes the final bill larger and the political maneuvering more toxic. This instability ensures that healthcare costs remain a defining, unresolved political battle for the next decade.

Gallery

Frequently Asked Questions

What exactly are the expiring ACA tax credits?

These are enhanced premium tax credits made available under recent legislation that cap the amount individuals pay for ACA marketplace health insurance premiums relative to their income. They were set to expire, meaning premiums would jump significantly for those relying on the enhanced subsidy levels.

Why are these expiring credits a major issue for the 2026 elections?

If the credits lapse, millions of middle-income Americans will face unaffordable premiums, creating an immediate economic crisis that will mobilize voters against the party perceived as responsible for allowing the subsidies to end.

Is healthcare cost inflation slowing down?

While overall inflation has cooled, healthcare costs—especially insurance premiums and out-of-pocket spending—continue to rise faster than wages, putting sustained pressure on household budgets, as highlighted by the KFF data.

What is the 'Unspoken Truth' about the ACA subsidies?

The unspoken truth is that the current enrollment success is built on a temporary financial patch, not sustainable pricing. The system is structurally dependent on these subsidies, making any lapse a guaranteed political and economic shock.