Micron's $100 Gamble: Why the AI Chip Boom Hides the Real Semiconductor Debt Bomb

Forget the hype. Micron Technology stock's 1-year outlook isn't about AI memory; it's about geopolitical risk and the hidden leverage in DRAM cycles.

Key Takeaways

- •Micron's valuation relies too heavily on uninterrupted AI spending, ignoring cyclical risks.

- •High CapEx requirements make Micron vulnerable to future ASP declines in commodity DRAM.

- •Geopolitical factors and subsidies introduce unpredictable regulatory risk.

- •Expect stock stagnation or decline within 12 months as inventory correction hits broader markets.

The Hook: The Illusion of the AI Gold Rush

Everyone is fixated on the soaring stock price of Micron Technology ($MU) and its role in the Artificial Intelligence (AI) revolution. They see High Bandwidth Memory (HBM) as a guaranteed rocket fuel. But this is journalistic malpractice. The real story isn't the immediate AI demand; it’s the structural fragility underlying the entire memory market. Investors betting on Micron in the next year are betting on geopolitics and macroeconomic fragility more than they are betting on superior engineering.

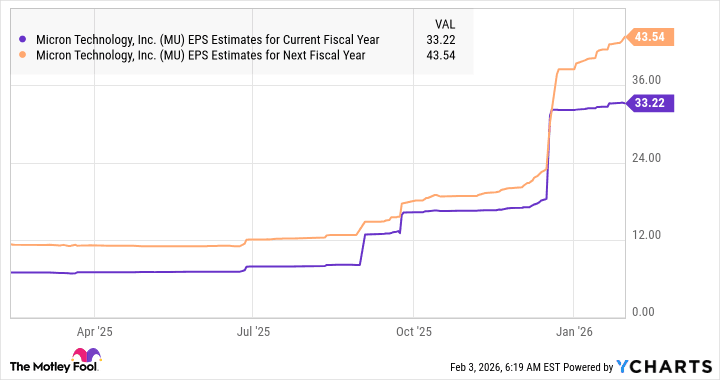

The consensus narrative, pushed by analysts who rarely look beyond the next earnings call, suggests Micron is perfectly positioned to capitalize on the insatiable need for faster DRAM and NAND. While technically true—demand is surging—this narrative ignores the semiconductor debt bomb ticking underneath the surface. This is the unspoken truth: the memory cycle is still a brutal, capital-intensive commodity game, and Micron’s massive capital expenditure (CapEx) required to stay competitive is a gigantic liability when the inevitable downturn hits.

The Deep Dive: Who Really Wins When HBM Goes Vertical?

HBM is undoubtedly lucrative, but it is not a moat. It’s a high-margin temporary advantage. The true winners in the short term are the foundries and the high-end GPU designers who dictate the terms. Micron is desperately playing catch-up to SK Hynix in the HBM3/HBM3E race. Their success is predicated on flawless execution *and* the sustained, irrational spending habits of hyperscalers like Nvidia and Microsoft.

Consider the leverage. Memory fabrication requires billions in upfront investment. When the market inevitably rebalances—and it always does—the companies with the highest debt load and the most aggressive expansion plans feel the knife first. Is Micron structurally sound enough to withstand a sudden 20% drop in average selling prices (ASPs) for standard DRAM, a common occurrence in past cycles? The faith being placed in their stock right now assumes perpetual, uninterrupted AI spending, which is a historical anomaly.

Furthermore, the biggest risk isn't competition; it’s supply chain nationalism. As semiconductor manufacturing becomes a strategic national security issue, government subsidies (like the CHIPS Act) distort natural market dynamics. While this offers short-term boosts for building domestic fabs—a key factor for any US semiconductor company—it also means that future profitability is increasingly tied to political lobbying rather than pure market efficiency. This adds a layer of unpredictable regulatory risk that standard valuation models cannot capture.

What Happens Next? The Contrarian Prediction

In 12 months, Micron’s stock price will likely be bifurcated. The first half of the year will see continued euphoria fueled by HBM capacity announcements. However, by Q4 of next year, we will see the first significant signs of inventory correction in the broader PC and smartphone markets, which still constitute the bulk of Micron’s revenue base. This correction will put immense pressure on their standard DRAM pricing.

My prediction is that Micron stock will trade sideways to down by the end of the one-year window, not because AI demand collapses, but because HBM saturation begins to erode margins faster than the market anticipates, forcing them to write down older inventory. The market is currently pricing in a perfect, uninterrupted upward trajectory for memory chip stocks. When that trajectory inevitably flattens due to commodity pricing pressure, the correction will be sharp. The real winners will be the disciplined, less leveraged players who can pivot manufacturing capacity quickly, not necessarily the ones making the loudest AI announcements today.

Key Takeaways (TL;DR)

- The current valuation heavily discounts the historical volatility of the memory cycle.

- Geopolitical subsidies mask underlying capital expenditure risks.

- HBM margins are temporary; competition is rapidly closing the technological gap.

- The risk of inventory correction in legacy markets remains high.

Gallery

Frequently Asked Questions

Is Micron Technology a good long-term investment despite cyclical concerns?

Long-term viability depends on their ability to maintain technological leadership in advanced packaging for HBM, but short-to-medium term performance is highly susceptible to the traditional memory cycle pressures.

What is the primary risk facing Micron stock in the next year?

The primary risk is the market overestimating sustained HBM pricing power while simultaneously underestimating the impact of inventory overhang in the non-AI segments like PCs and smartphones.

How does the CHIPS Act actually impact Micron's profitability?

The CHIPS Act provides crucial funding for domestic fab construction, lowering the effective cost of building advanced facilities, but it also ties future revenue streams more closely to U.S. government policy and national security priorities.

What is the difference between DRAM and HBM in the current market?

DRAM is the standard, high-volume memory used in PCs and phones, subject to commodity pricing. HBM (High Bandwidth Memory) is specialized, stacked memory essential for AI accelerators, commanding premium pricing due to its complexity and scarcity.

Related News

The Oregon Auto Show's Tech Mirage: Why Today's 'Innovation' is Tomorrow's Obsolete Hardware

The Oregon International Auto Show is back, but is it showcasing true automotive technology breakthroughs or just selling shiny distractions? We analyze the real winners.

The AI Mirage: Why Your 'Smart' Tools Are Actually Just Expensive Consultants for the Elite

Forget the hype. The true cost of artificial intelligence isn't computational power; it's the centralization of decision-making power.

The GPUaaS Lie: Why On-Prem AI Infrastructure Is Actually A Vendor Lock-In Trap

The rush to build **on-prem AI infrastructure** using **GPUaaS** models isn't about control—it's about a new form of dependency. Analyze the hidden costs.